Categories

All About Texas, Real Estate Market StatisticsPublished November 7, 2025

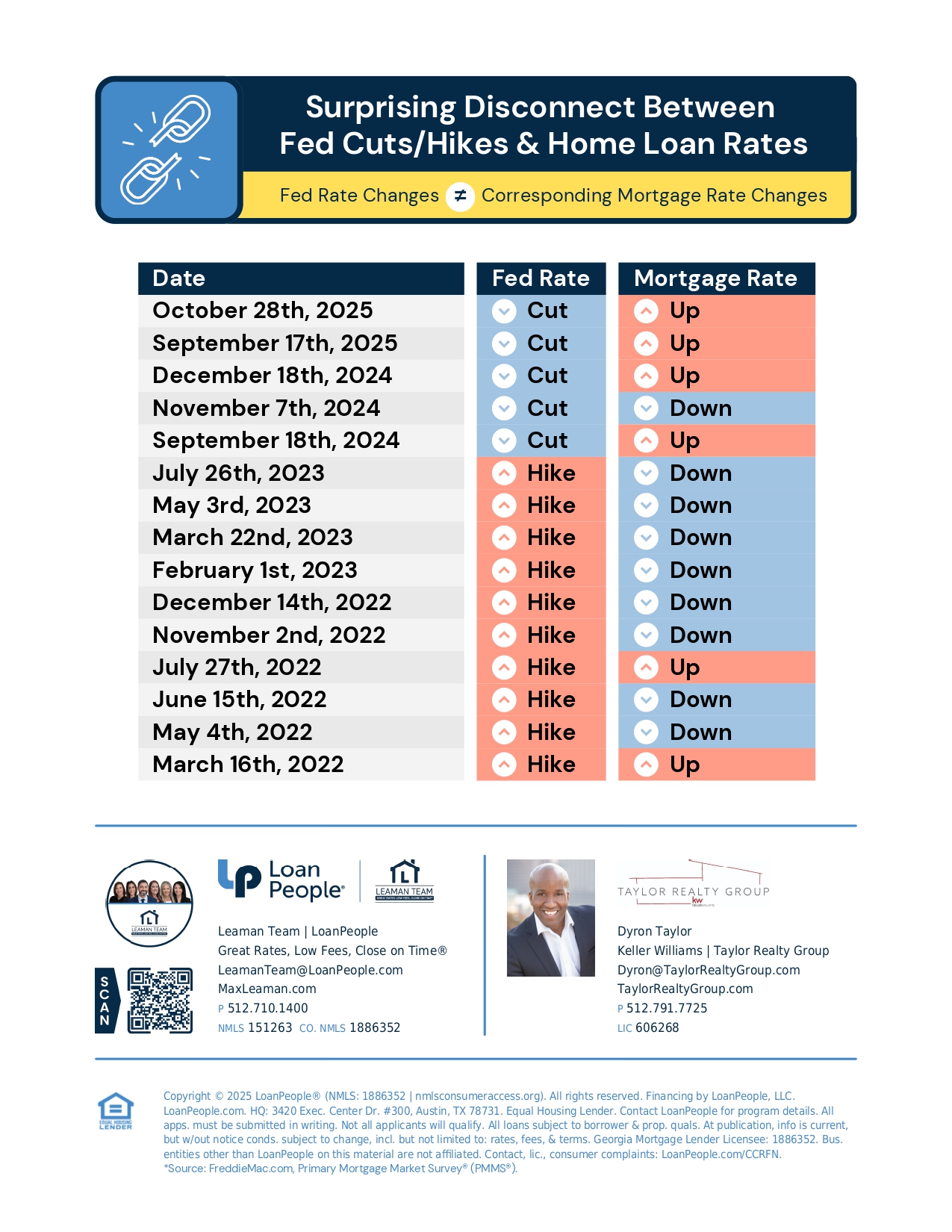

The Surprising Truth: Why Fed Rate Changes Don't Control Your Mortgage Rate

The Mortgage Rate Myth

It's one of the biggest misconceptions in finance: when the Federal Reserve cuts its rate, mortgage rates fall; when the Fed hikes rates, mortgage rates rise.

Our infographic shows that the opposite is often true, revealing a surprising and powerful disconnect between the Fed’s actions and what you pay for a 30-year fixed mortgage.

The Real Drivers of Mortgage Rates

The key reason for this split is simple: the Fed Funds Rate only controls short-term loans (like credit cards and HELOCs).

The 30-Year Fixed Mortgage Rate is a long-term loan tied to the 10-Year Treasury Yield. This yield is driven by bond market investors who are betting on the future:

- Future Inflation: If the bond market fears inflation, mortgage rates go up, regardless of what the Fed does today.

- Anticipation: The market often prices in a Fed hike or cut long before it happens. This explains why we often see mortgage rates drop after an expected Fed hike—the "bad news" was already accounted for.

What the Data Shows

The data here clearly proves the point:

- In several instances in 2022 and 2023, the Fed was aggressively Hiking rates, yet mortgage rates moved Down.

- In the future projections shown, the Fed Cuts rates, but mortgage rates jump Up.

The Bottom Line: Don't wait for the Fed to act before you buy or refinance. The bond market moves on its own schedule. Talk to a mortgage

|

or another way